The Edges of New Zealand's AI Energy Blueprint Are Forming

AI is becoming infrastructure - but infrastructure alone doesn’t create value. As energy, compute, and capital begin to align, a new architecture is forming beneath the surface of the economy. The question is whether New Zealand can connect it fast enough to capture new global value.

Part of a broader body of work on how AI, infrastructure, and capability are reshaping New Zealand’s future.

From AI as technology to energy-driven infrastructure - and why it changes how New Zealand creates value

What if New Zealand doesn’t have an AI strategy problem at all?

What if the real issue is that we’ve been looking in the wrong place for it?

Because if you step back - past the AI tools, past the policy papers - something else is starting to form.

Not a strategy.

An energy blueprint.

And more specifically:

A global energy-to-compute ecosystem.

One that is already reshaping how economies grow.

And one that New Zealand is beginning to enter.

The Misread: Thinking This Is About AI

Most conversations about AI still start in the same place:

Models.

Tools.

Adoption.

But that frame is already outdated.

Because AI is no longer just a technology layer.

It’s becoming core infrastructure.

But infrastructure doesn’t create value on its own.

Value comes from how it connects into the wider system around it:

Energy.

Transmission.

Data.

Capital.

Governance.

This is where Darryl Munro’s critique on the NZ-EOS framework lands cleanly.

And he’s right...

The New Zealand Economic Operating System is useful.

It gives us a map and a shared system language.

But the real test for New Zealand is not the system map.

It’s the machine room.

The part where strategy turns into reality -

where energy gets generated, infrastructure gets built, capital gets deployed, and things actually operate in the real world.

Can we actually build the thing?

The Invisible Layer Is Becoming Visible

For a long time, energy sat in the background.

Reliable. Assumed. Invisible.

Until it isn’t.

Because something has changed.

Compute now requires energy at scale.

And intelligence now requires compute.

Which means:

Energy is becoming a proxy for growth.

And the numbers are starting to show it.

New Zealand already generates around 43,900 GWh of electricity each year, with roughly 85% coming from renewable sources.

That’s not just good.

That’s globally unusual.

It’s a structural advantage.

But now, at this moment, this is where things start to accelerate.

Demand is about to surge.

MBIE modelling suggests electricity demand could grow between 35% and more than 80% by 2050, pushing total consumption toward ~62–72 TWh, with peak demand rising to ~9–12.5 GW.

That’s not incremental change.

That’s system-level pressure.

When Compute Starts Pulling on the Grid

The easiest way to understand what’s happening is this:

AI doesn’t just run on software.

It runs on electricity - on electrons moving through physical infrastructure.

And it requires them at a scale we have not had to plan for before.

New Zealand’s own projections now treat data centres as a major new source of electricity demand.

By 2030:

• data centres could consume around 1.8 TWh of electricity

• in higher scenarios, demand could rise to around 4.6 TWh

(MBIE, Electricity Demand and Generation Scenarios 2024)

At the upper end, that’s roughly equivalent to Tiwai Point - the aluminium smelter, and one of the largest single electricity users in New Zealand.

That gives a sense of scale.

Not just for the sector overall…

but for what a single large facility, or cluster of them, can represent on the grid.

And the pipeline signals are even clearer:

Around 64% of new large electricity loads being proposed are tied to this category.

This is no longer marginal demand.

This is system-shaping demand.

The Energy Architecture Starts to Rewire

When compute demand increases - energy demand rises.

When energy demand rises - grid constraints emerge.

When grid constraints emerge - investment shifts.

And when investment shifts - geography changes.

You can see that change now being acknowledged from inside the energy sector itself.

As Transpower’s John Clarke puts it:

“Electricity is a major enabler of economic growth.”

It’s a relatively simple line. But it reframes everything.

Energy is no longer just supply.

It’s capability.

Making It Real: What’s Actually Being Built

This isn’t theoretical. It’s already happening.

Take Southland, for example.

On the surface, it’s a region with strong renewable energy.

But underneath - it’s becoming something else.

A potential compute hub.

One of the clearest signals comes from Datagrid.

Instead of positioning itself as just another data centre provider, it’s framing its development as an:

“AI factory.”

In simple terms:

It takes electricity - and turns it into AI computation at scale.

The ambition is significant.

A proposed ~280 MW compute campus at Makarewa, near Invercargill, powered by renewable energy, supported by new subsea connectivity through the proposed Tasman Ring, and anchored by a ~140 MW power agreement with Mercury.

In plain English:

Take abundant renewable energy.

Plug it directly into large-scale AI infrastructure.

And sell that compute to the world - for AI training, models, and workloads.

This is a different layer of capability - but one that sits alongside domestic AI development.

It’s not just about skills, talent, or local AI-native software companies building on top of AI.

It’s about turning energy into exportable compute capacity -

where other countries and companies pay to use the infrastructure we host.

This is no longer just a traditional data centre model.

Historically, data centres stored and served data.

But AI infrastructure changes the role of the data centre itself.

Electricity is transformed into globally consumed computation - powering models, training systems, and AI workloads at industrial scale.

In this new world, energy itself starts becoming part of the export system.

Meanwhile, the Rest of the Energy Sector Is Moving

Across the country, the energy base is already strong.

Generation is still dominated by:

Meridian Energy.

Mercury.

Contact Energy.

Genesis Energy.

Contact’s acquisition of Manawa Energy in 2025 is part of this changing infrastructure picture.

Manawa was the former Trustpower generation business. With the acquisition now complete, Contact has become a larger and more systemically important electricity infrastructure owner, combining geothermal, hydro, gas-fired firming, storage, solar, battery, and retail capability across a broader platform.

The significance is that New Zealand’s energy transition is not only about building more renewables.

It is also about who owns and coordinates the flexible infrastructure that keeps the system reliable as demand grows from electrification, data centres, cloud infrastructure, and AI-era compute loads.

At the same time, a newer layer of renewable infrastructure development is also forming around growth-oriented generation and storage platforms, including:

Lodestone Energy.

Rānui Generation.

And other renewable, storage, and development platforms.

Together, these developments point toward something larger:

the rapid expansion of renewable infrastructure designed for an increasingly electrified and compute-intensive economy.

And the real signal is in what’s being built next.

The development pipeline now includes:

• roughly 289 proposed generation projects

• totalling around 44 GW of capacity

• with more than 80% in renewables

Much of it is:

Wind.

Solar.

Solar paired with battery storage.

Not all of this will be built.

But that’s not the point.

The point is direction.

Capital is moving toward flexible, renewable, AI-compatible energy infrastructure.

The Uncomfortable Truth

The uncomfortable truth is this:

New Zealand doesn’t have a simple energy shortage -

it has an energy network that struggles to deliver power where and when it’s needed.

That’s the challenge today.

What comes next is different.

It’s no longer just about delivery.

Generation is growing.

Demand is accelerating.

Infrastructure is evolving.

It’s about scaling the network for the intelligence era -

where compute, data centres, and AI infrastructure drive entirely new levels of demand.

And at that scale, the real constraint becomes clear:

New Zealand has a coordination problem.

And that gap - between capability and coordination - is where value is either created…

or lost.

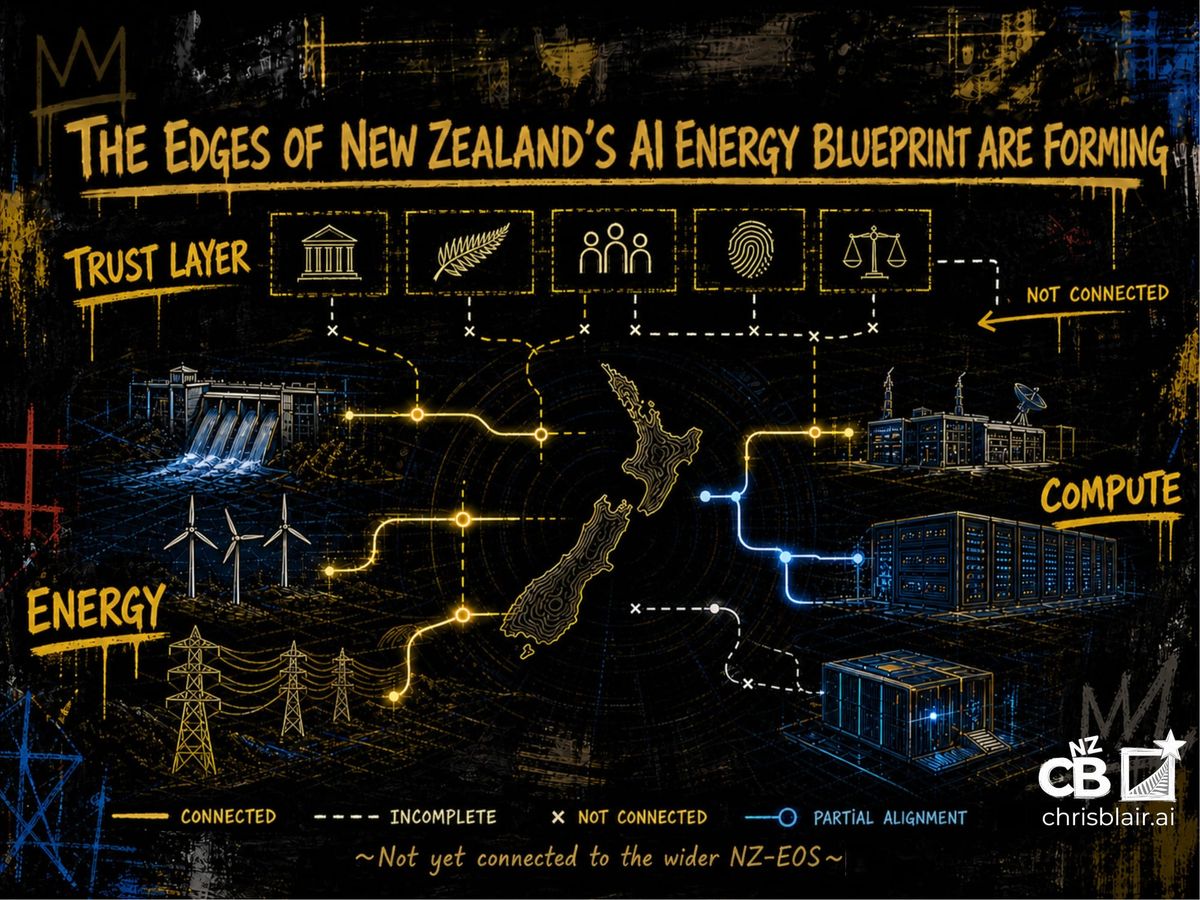

The Stack That’s Actually Forming

If you map what’s happening around the world, a pattern emerges.

Generation. Grid. Compute. Infrastructure. Silicon.

And New Zealand sits in a very specific position inside that stack.

Not at the extremes.

But in the middle.

Which is exactly where the leverage is.

And critically - this change is now being acknowledged in forward planning.

As Transpower’s David Knight noted in their latest electrification outlook:

“Data centres… could materially shift the future of energy demand in New Zealand.”

That’s part of the bridge New Zealand now needs to build.

But it’s not enough on its own.

We also need to wrap a broader economic operating system around it - one that connects infrastructure, capability, and value creation across the country.

From energy to AI.

From infrastructure to economic architecture.

The Missing Layer - And New Zealand’s Real Advantage

Up to this point, the New Zealand AI energy blueprint looks like this:

Energy.

Compute.

But that’s not where we should stop -

not if we want to build an economy capable of doubling New Zealand’s exports over the next decade, and lifting long-term prosperity as a result.

Because compute alone doesn’t create that kind of economic value.

It needs to connect into a broader economic operating system - the NZ-EOS:

Capital.

Capability.

Research.

Industry.

Data.

Governance.

Export pathways.

And within that system, one pillar becomes especially important.

Trust.

In a global AI economy, countries won’t just compete on who has compute.

They’ll compete on where data can be trusted,

where AI can be governed,

and where digital and AI systems are safe to operate.

This is where New Zealand has a unique and under-recognised position.

A trusted operating environment.

Anchored in:

Strong governance.

Trusted institutions.

And frameworks like Te Mana Raraunga.

Frameworks that ensure data governance reflects:

Indigenous rights.

Long-term stewardship.

And the ethical use of data and AI systems.

Not only as a compliance layer.

But as system architecture.

And in a global AI economy, that becomes a selection criterion for:

Where data is hosted.

Where models are trained.

Where AI systems are deployed.

Which means New Zealand’s stack becomes:

Energy.

Compute.

A trusted operating environment - the layer that governs how data, AI systems, identity, assurance, and jurisdiction work together.

And that combination becomes more valuable in a world where trust, assurance, and jurisdiction are becoming selection criteria.

The Real Constraint

At this point, the constraint becomes clear.

It’s not energy.

It’s not capital.

It’s coordination.

Because when these layers don’t align:

Energy gets built without demand.

Compute gets built without power.

Data gets hosted offshore - and the compute follows.

Full value doesn’t get created.

It leaks.

The Moment for Opportunity

This is where the implications start becoming tangible.

For organisations:

Energy is no longer just a cost line.

It’s a strategic input.

For industries:

AI advantage will not come from tools alone.

It will come from access - to compute, energy, and a trusted operating environment.

For New Zealand:

The long-term opportunity is not just renewable energy.

It’s the combination of:

Low-carbon energy.

AI infrastructure.

A trusted operating environment.

Because over the next decade, countries will not compete on AI models alone.

Countries will compete on:

Energy availability.

Infrastructure.

Data governance.

Trust itself.

Which means:

Energy becomes economic policy.

Compute becomes industrial strategy.

Trust becomes competitive advantage.

The Open Question

So the question is no longer:

Do we need an AI strategy?

The real question is whether New Zealand can connect:

1. The operating system.

2. The machine room.

3. And the trust layer.

Fast enough to matter?

Because the edges are already forming.

The signals are there.

The infrastructure is moving.

The opportunity is real.

But only if we choose to see it clearly,

and act in coordination.

Selected References

Electricity Demand and Generation Scenarios (MBIE, 2024)

New Zealand’s long-term electricity demand and generation modelling.

Electricity Demand and Generation Scenarios 2024 Report (PDF)

Detailed assumptions, scenarios, and projections underpinning national energy forecasts.

Transpower Electrification Outlook

National grid perspective on future electricity demand and system transformation.

The Future of New Zealand Data Centre Exports (BCG)

Analysis of New Zealand’s potential role in global compute and data centre infrastructure.

Related Essays

AI Is Becoming Core Infrastructure

New Zealand’s Missing AI Infrastructure

Redesigning New Zealand’s System for AI-Enabled Growth